Although reverse factoring and traditional factoring both involve accelerating invoice payments, they differ fundamentally in structure, motivation, and risk allocation. Understanding these differences is essential for business owners, consultants, and brokers navigating modern working capital solutions.

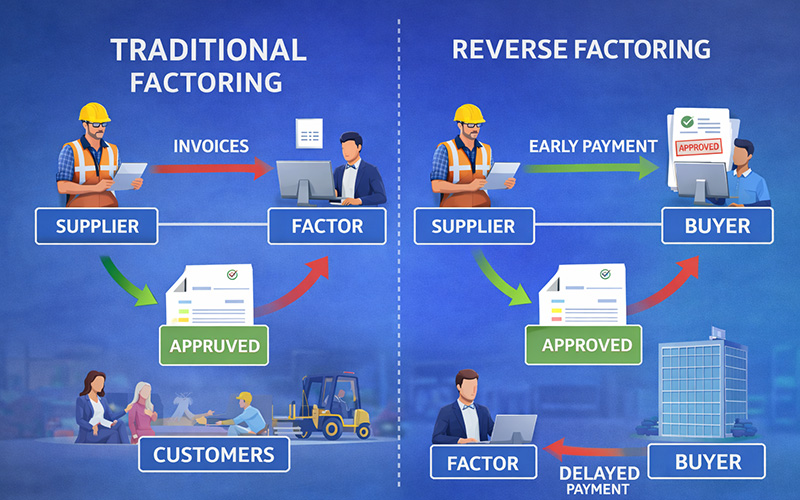

In traditional factoring, the supplier initiates the transaction. A business sells its invoices to a factor to obtain immediate cash, typically because it needs working capital to fund operations or growth. The factor evaluates the supplier’s customers individually, pricing the transaction based on customer credit quality, invoice volume, and industry risk. The supplier controls when and how factoring is used.

Reverse factoring turns this model upside down. The transaction is initiated by the buyer, not the supplier. The buyer establishes a financing program and invites suppliers to participate. Once the buyer approves an invoice, payment risk shifts almost entirely to the buyer, since the buyer has already acknowledged its obligation to pay. As a result, the factor’s underwriting focuses primarily on the buyer’s creditworthiness.

Another key distinction lies in purpose. Traditional factoring is primarily a supplier cash-flow solution. Reverse factoring is both a financing tool and a strategic supply-chain management solution. Buyers use reverse factoring to reduce supplier stress, prevent disruptions, and gain commercial advantages such as better pricing, reliability, and priority fulfillment.

For brokers and consultants, these differences affect deal sourcing. Traditional factoring opportunities are usually identified at the supplier level—small and mid-sized businesses struggling with cash flow. Reverse factoring opportunities, however, often emerge from conversations with large buyers, procurement teams, CFOs, and operations executives who are focused on stabilizing and optimizing their supplier ecosystems.

Both models play important roles in alternative finance, but reverse factoring represents a more strategic, relationship-driven evolution of the factoring concept.